Table of Contents

- Why Fintech Listing Execution needs Higher Standards

- Implementation Checklist from Kickoff to Stable Operations

- Fintech-Specific Risk Controls

- Common Mistakes when Choosing Fintech Listing Services

- 90-Day Fintech Directory Plan

- FAQ

sbb-itb-8e44301

Quick Answer

Fintech startups directory listing services deliver better outcomes when the work is run as a controlled growth workflow, not a volume campaign. The best fintech teams publish to a focused set of high-fit platforms, validate profile quality early, and expand only after quality and maintenance signals are stable.

A practical 2026 sequence is:

- define one canonical fintech profile baseline,

- score candidate directories by buyer fit and profile quality,

- launch a small first wave with strict QA,

- scale only when correction load stays predictable.

This approach usually beats broad submission because fintech categories are trust-sensitive. Low-quality or inconsistent listings can reduce credibility faster than they increase visibility.

Why Fintech Listing Execution needs Higher Standards

Fintech products are often evaluated with extra scrutiny. Buyers and partners check brand consistency, positioning clarity, and trust signals across multiple channels before signup or contact. Directory profiles are part of that validation path.

That is why fintech teams should not use a generic seo directory list without filtering. A list can be a useful source, but the active portfolio should be selected with tighter standards:

- audience relevance to fintech buyers,

- profile depth for product context,

- update and correction control,

- realistic maintenance burden.

When this discipline is missing, teams usually run into:

- inconsistent positioning across platforms,

- profile drift between launches,

- duplicate entries that weaken trust,

- rising operational overhead with unclear ROI.

The goal is not just more listings. The goal is a reliable listing system that supports growth and trust at the same time.

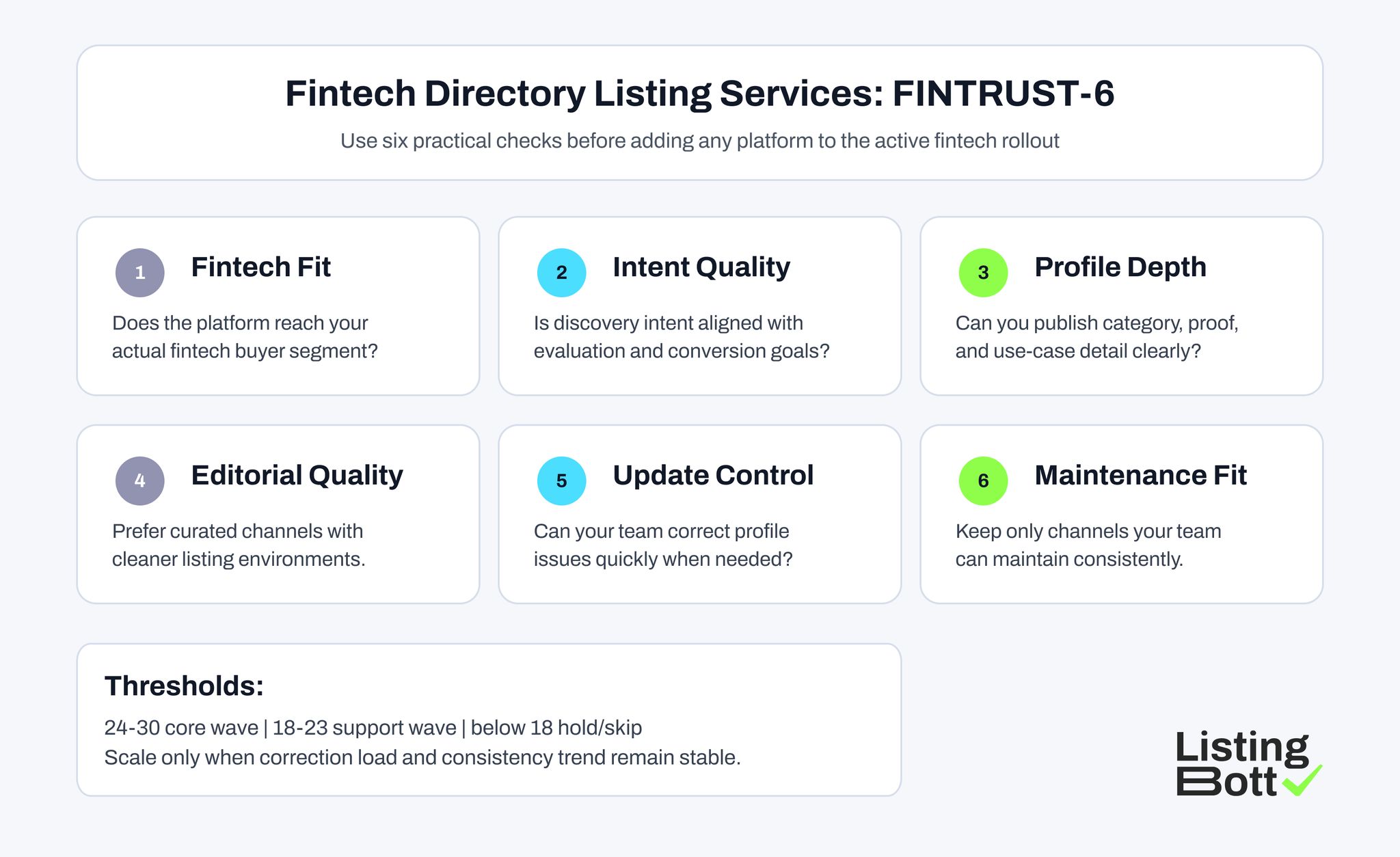

The FINTRUST-6 Model for Selecting Fintech Directory Services

Use this six-factor model to rank channels before launch.

| Factor | Practical question | Why it matters | Score (1-5) |

| Fintech audience fit | Do decision-makers in your target segment use this platform? | improves relevance and conversion potential | 1-5 |

| Intent quality | Is user intent aligned with fintech product discovery or evaluation? | filters low-intent traffic sources | 1-5 |

| Profile depth | Can you clearly explain product category, use cases, and proof? | supports trust and buyer qualification | 1-5 |

| Editorial cleanliness | Is platform quality controlled and reasonably curated? | reduces noisy context risk | 1-5 |

| Update control | Can your team fix critical profile issues quickly? | protects consistency over time | 1-5 |

| Maintenance efficiency | Can this channel stay accurate without constant manual overhead? | keeps operations scalable | 1-5 |

Suggested thresholds:

- 24-30: core wave,

- 18-23: support wave,

- below 18: hold/skip.

This scoring method gives fintech teams a practical way to evaluate business directories for seo opportunities without turning every directory into an active channel.

Fintech Directory Listing Services: FINTRUST-6

Best-fit Listing Platforms for Fintech Startups Directory Listing Services

This platform set combines fintech-relevant discovery channels and high-utility startup directories.

| Platform | URL | Why it is a best fit | Ideal company profile | Submission note |

| GrowthList | https://growthlist.co/fintech-startups/ | Focused fintech startup discovery context with category relevance | fintech startups seeking targeted visibility | keep positioning clear by problem/use-case, not only feature list |

| Fintech Marketing Community | https://fintechmarketingcommunity.com/solutions | Fintech-focused ecosystem exposure and niche audience alignment | early to growth-stage fintech brands | maintain clear audience and product message consistency |

| Crunchbase | https://www.crunchbase.com/ | Strong company discovery and entity-profile visibility layer | funded startups and B2B fintech companies | keep funding, category, and company description accurate |

| Wellfound | https://wellfound.com/ | High startup ecosystem visibility and brand credibility support | venture-backed and talent-scaling fintech startups | align brand profile with latest product positioning |

| Product Hunt | https://www.producthunt.com/ | Launch and discovery channel for product-led fintech tools | product-led fintech SaaS and AI-fintech tools | prepare launch copy and proof points in advance |

| G2 | https://www.g2.com/ | High-intent software discovery and comparison context | B2B fintech software providers | complete category mapping and profile depth fields |

| Capterra | https://www.capterra.com/ | Strong buyer research behavior for software evaluation | fintech SaaS vendors targeting operations or finance teams | keep descriptions outcome-focused and specific |

| GetApp | https://www.getapp.com/ | Useful software directory visibility in mid-funnel discovery | SMB-focused fintech software products | keep pricing and feature summary aligned with landing pages |

| BetaList | https://betalist.com/ | Early traction channel for startup visibility | pre-seed and seed fintech products | use concise differentiation statement and clean onboarding link |

| F6S | https://www.f6s.com/ | Startup ecosystem exposure with founder/investor touchpoints | accelerator-linked and fundraising-stage fintech startups | keep profile status updated to avoid stale entries |

How to apply this list:

- choose 5-6 channels for the core wave,

- keep the rest as conditional support,

- expand only after quality gates pass.

Core Wave Design for Fintech Teams

For fintech startups, first-wave composition should balance trust, discovery intent, and maintenance load. A strong core wave often includes:

- one or two fintech-focused niche channels,

- two startup ecosystem channels,

- two high-intent software directories (if product category fits).

The reason this works is simple. It gives you channel diversity without creating immediate maintenance sprawl.

Practical first-wave checklist:

- confirm profile baseline and messaging hierarchy,

- map each platform to one target audience segment,

- define owner for launch and owner for corrections,

- schedule a QA review window 7-14 days post-launch.

This keeps local and broad directory execution in sync, which is important if you also maintain local business directory listings for geo visibility.

Service Model Comparison for Fintech Directory Work

Teams evaluating fintech startups directory listing services usually compare four execution models.

| Model | Best for | Main risk | What to validate |

| Manual founder-led workflow | very early stage teams with narrow scope | inconsistency when priorities shift | owner capacity and checklist rigor |

| Freelancer support | short launch windows | variable quality standards | revision process and QA ownership |

| Agency-managed execution | teams wanting outsourced throughput | process quality differs by provider | channel selection logic and reporting depth |

| Tool-led controlled workflow | teams scaling repeatable submissions | weak outcomes if governance is absent | baseline rules, QA cadence, and accountability |

For fintech, model quality matters more than speed alone. Fast submissions without stable controls often create expensive cleanup cycles later.

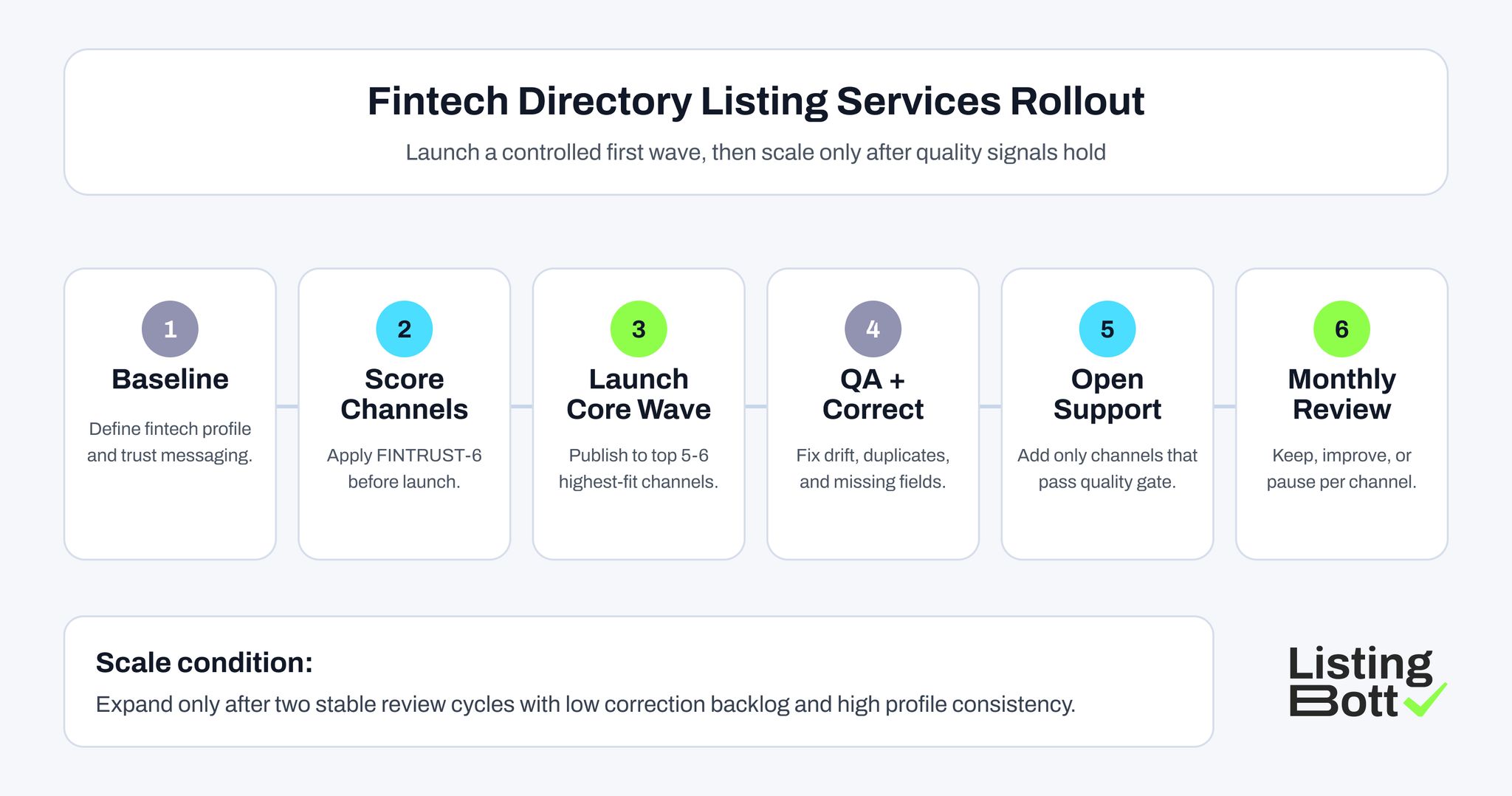

Fintech Directory Listing Services Rollout

Implementation Checklist from Kickoff to Stable Operations

Step 1: define canonical fintech profile pack

Include:

- approved company narrative,

- category mapping rules,

- product positioning by audience,

- destination URL map,

- proof and trust assets.

Step 2: score candidate channels

Run FINTRUST-6 scoring and classify channels into core, support, or hold.

Step 3: prepare launch assets once

Prepare reusable assets for every platform:

- short and long descriptions,

- category-specific copy variants,

- image/logo pack,

- core proof statements,

- internal QA checklist.

Step 4: launch core wave

Publish to selected core platforms and capture:

- submission date,

- live URL,

- approval status,

- assigned owner.

Step 5: run post-launch QA

Validate:

- profile consistency,

- category alignment,

- destination URL accuracy,

- duplicate risk,

- missing fields.

Step 6: close critical issues before scaling

Do not open support wave while critical mismatches remain unresolved.

Step 7: open support wave selectively

Add support channels only when two consecutive review cycles show stable quality.

Step 8: run monthly channel decisions

For each active platform, choose:

- keep,

- improve,

- pause.

This workflow keeps free online business directories from becoming a long-term maintenance trap.

KPI Board for Fintech Listing Performance

Measure outcomes with channel-level clarity.

| KPI | Why it matters | Healthy signal | Risk signal |

| Profile consistency rate | indicates data reliability | 95%+ and stable | repeated critical mismatches |

| Correction closure time | reflects operational control | predictable closure cycle | growing aged backlog |

| Duplicate profile rate | shows hygiene quality | low and declining | repeated duplicate emergence |

| Channel contribution quality | checks relevance of visits and actions | stable high-intent engagement | low-intent sessions dominate |

| Maintenance load ratio | tracks scalability of process | controlled effort per cycle | rising effort without quality gain |

These metrics help decide which channels deserve continued investment.

Fintech-Specific Risk Controls

Fintech teams should add extra controls to reduce trust risk:

1) Positioning consistency control

Keep product category and core message aligned across all listings. Conflicting positioning weakens credibility and confuses buyers.

2) Destination-page alignment control

Map each listing to the most relevant page, not always to homepage. Better mapping usually improves qualification quality.

3) Fast correction path

Define who fixes errors and within what SLA. In trust-sensitive categories, slow corrections can damage first impressions.

4) Duplicate suppression routine

Run periodic duplicate checks and resolve conflicts early, especially after large update waves.

5) Expansion gate

Require two stable review cycles before adding more channels.

6) Quarterly de-prioritization review

Pause channels with high load and weak contribution even if they are part of legacy lists.

These controls make a major difference between sustainable growth and ongoing cleanup work.

Common Mistakes when Choosing Fintech Listing Services

1) Choosing by volume promise only

High submission counts can look attractive but often hide quality and maintenance risks.

2) Using generic templates without fintech positioning

If profile copy ignores category nuance, intent match and credibility usually drop.

3) Expanding before QA stability

Adding channels before corrections are controlled increases operational debt.

4) Treating all directories as equal

Directory utility varies widely. Fit-based scoring is mandatory.

5) No channel retirement rule

Without a pause policy, low-value channels consume time indefinitely.

6) Reporting only launch counts

Submission volume does not show whether listings are helping growth.

7) Ignoring local visibility layer

Some fintech teams skip local coverage entirely, even when geo trust signals matter for their acquisition strategy.

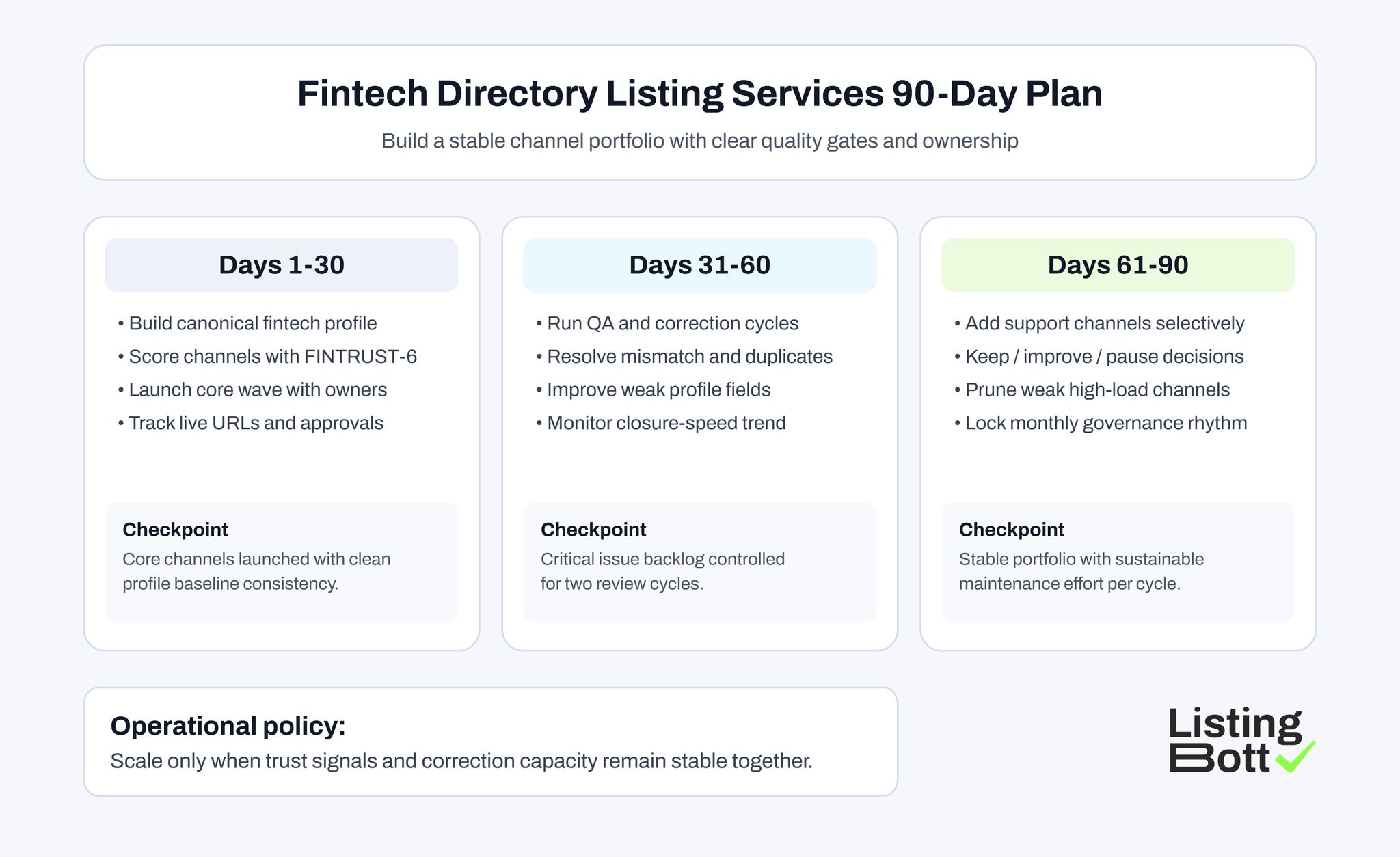

90-Day Fintech Directory Plan

Days 1-30: foundation

- build canonical profile pack,

- complete FINTRUST-6 scoring,

- launch core wave,

- assign ownership.

Days 31-60: stabilization

- run QA cycles,

- close critical mismatches,

- fix duplicates,

- improve weak profiles.

Days 61-90: scale and optimize

- open support wave if quality gates pass,

- pause weak channels,

- refine destination mapping,

- lock monthly review rhythm.

By day 90, the goal is a portfolio you can maintain confidently, not just a longer channel list.

Fintech Directory Listing Services: 90-Day Plan

Execution note: For founder-led teams with limited bandwidth, it is better to run a smaller high-fit channel set with consistent monthly QA than to chase broad coverage that cannot be maintained.

Where ListingBott Fits

ListingBott supports structured directory publication and tracking for teams that want repeatable execution.

Typical flow:

- onboarding details are collected,

- listing scope is approved,

- publication is executed,

- reporting is delivered.

Offer alignment:

- one-time payment model,

- publication to 100+ directories,

- no hidden extra fees,

- refund possible if process has not started.

Promise limits:

- no guaranteed ranking position,

- no guaranteed traffic by a specific date,

- no guaranteed indexing speed,

- no guaranteed outcomes controlled by third-party platforms.

Qualified DR statement: DR growth to 15 can be promised only when starting DR is below 15, the selected goal is domain growth, and the approved listing set is in place.

FAQ: Fintech Startups Directory Listing Services

How many platforms should a fintech startup launch first?

Most teams should start with 5-6 high-fit platforms in a controlled first wave, then expand only after quality metrics stabilize.

Are fintech-specific directories better than general startup directories?

They serve different roles. Fintech-specific channels improve niche relevance, while broader startup and software directories can expand discovery reach.

Should we prioritize free directories first?

Use fit and quality as primary filters. Some free online directory listings are useful, but they should pass the same quality gates as paid options.

Can directory listing services guarantee ranking outcomes?

No. Listings support visibility and trust signals, but rankings depend on broader SEO execution .

Is this only for startups, or also for scale-ups?

The framework works for both. Scale-ups usually add stricter ownership, reporting, and de-prioritization controls as channel count increases.